London, 9 July 2026 – The global 3D printer

market experienced robust growth in the first quarter of 2026,

driven by an explosive Entry-level segment and accelerating demand

for high-end Industrial systems. According to the latest analysis by

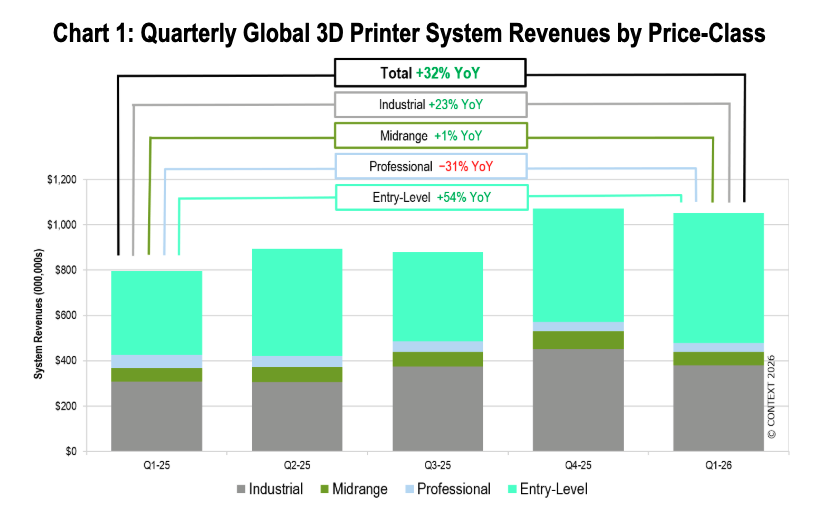

global market intelligence firm CONTEXT, the industry enjoyed a +32%

year-on-year (YoY) gain in total hardware system revenues. Most of

the growth came by way of accelerated Entry-level shipments, with a

+39% unit growth translating into a +54% surge in revenues.

Additionally, Industrial revenues rose nicely, up +23% from a year

ago on the back of an +18% increase in unit shipments.

"The current market presents a disparate

demand outlook," said Chris Connery, VP of Global Analysis at

CONTEXT. "While some vendors report exceptionally strong demand,

especially related to global conflicts and defence initiatives, others

report challenges associated with the many unknowns including ongoing

global conflicts, fears of rising inflation, higher interest rates

impacting capital investments, and a sluggish European economic

environment. However, the strong performance of the Industrial sector,

marking its third consecutive quarter of growth after two years of

declines, is a clear indicator of the technology's continued

integration into volume production.”

Industrial Systems

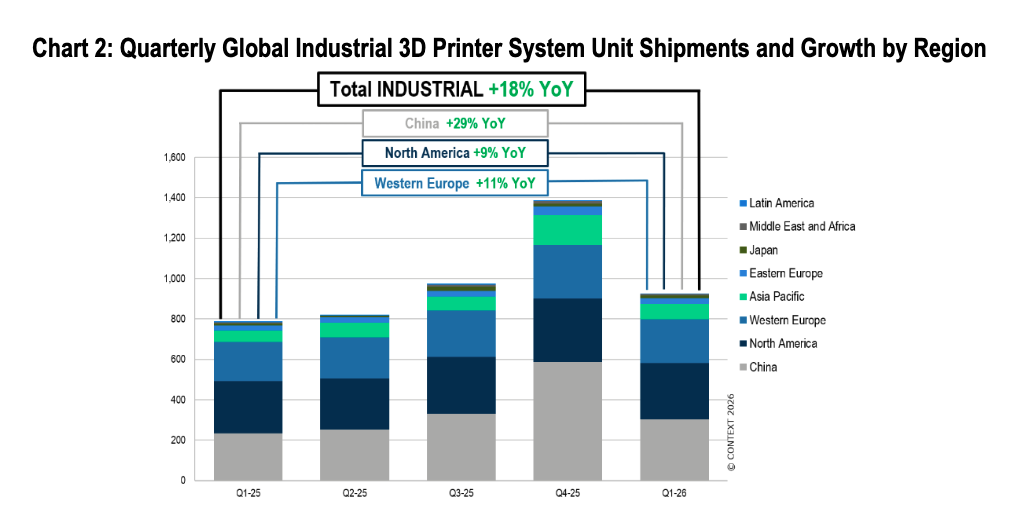

Global shipments of Industrial price-class

systems (>$100K) were up +18% in Q1-26. Nine out of the top ten

global vendors shipped more units in Q1-26 than a year ago and

Industrial shipments were up across all major regions: China +29%,

North America +9% and Western Europe +11%. China remains the world’s

largest market for Industrial 3D Printer system shipments, with most

of its demand fulfilled by domestic suppliers.

-

Metals:

Industrial Metal system shipments rose +10% YoY in Q1-26.

Powder Bed Fusion (PBF) remains the dominant technology,

accounting for 81% of the total Industrial Metals market,

with Metal PBF unit shipments up +24% YoY. Western leader

EOS had a strong quarter seeing its Metal shipments more than

doubled from a year ago, and separately announced the biggest

contract in its history, with a defence drone maker. Some reports

even indicate Metal PBF demand is outstripping supply in the West,

suggesting 2026 may be supply-limited as machine OEMs catch up on

production. In China, HBD, Farsoon and BLT all saw strong YoY

shipment growth with the latter two citing incredibly strong

demand in the 3C sector (Computer, Communication, and Consumer

Electronics.) This demand, strong in Q4-25 and carrying over into

Q1-26, was reportedly mostly for the production of titanium mobile

phone components, specifically hinges for foldable phones and

titanium smartphone frames. While such demand in China shifted the

overall market back toward lower-priced Metal PBF systems, other

vendors saw continued success with more advanced system sales.

Nikon SLM Solutions shipped more of its advanced, large

build-volume, multi-laser NXG systems than ever before, a +42% YoY

increase in unit shipments that put the company at the top of the

category's revenue leaders.

-

Polymers: Global shipments for Industrial Polymer

systems surged +31% YoY, heavily skewed by a massive shipment

acceleration from Carbon thanks to growing demand for

lattice-based consumer solutions (evidenced by their recent

announcement of relationship with DDK for the production of

bicycle saddles.) Excluding Carbon, Industrial Polymer shipments

were still up a healthy +14%. Additionally seeing growth in the

period was the Polymer Powder Bed Fusion space with global

shipments up +30% from a year ago thanks to strength from HP and

EOS, both of which saw shipments rise +100% from the year ago

quarter. Drone production remains a demand catalyst for Polymer 3D

printing. OEMs of Industrial Material Extrusion printers capable

of high-performance polymer processing, and of Polymer Powder Bed

Fusion systems, cited demand from this market as a driver of

shipment growth in the period. The period also saw one of its

global unit leaders in the Polymer machine space, UnionTech, issue

an IPO Prospectus in hopes of going public later this year on the

Hong Kong Stock Exchange.

Midrange and Professional Systems

The middle of the market (Professional + Midrange

price-classes) remained challenged mostly by the cannibalization of

Material Extrusion (FDM/FFF) demand by the Entry-level. That is

changing, though, as new product introductions and corporate

consolidation reshape the segment.

Midrange ($20K–$100K): Global shipments dropped

-6% YoY. The Polymer PBF sub-segment, however, is running hot, with

shipments up +48% YoY. This new Midrange price class for production

Polymer-PBF machines is becoming crowded: Formlabs has entered with

its newly announced Fuse X1, and HP has announced its forthcoming

sub-$60K Jet Fusion 1200. Both will join solutions from Raise3D, which

had strong initial shipments in the quarter as its market introduction

continued, and a range of others from vendors across the globe.

Professional ($2.5K–$20K): Shipments contracted

-22% YoY, and revenues fell -31%. New technology in this price class,

including Composites and full-colour Material Jetting, are set to

boost the segment in coming quarters. Composites look to get a lift

with Stratasys' planned acquisition of Markforged from Nano Dimension.

Entry-Level Systems

The Entry-level category (≤$2,500) alone

accounted for 54% of all 3D printing system revenues in the period.

Global shipments were up +39% YoY. China has become to the consumer

3D printing market what Japan was to consumer electronics in the

1980s: almost all of the ingenuity, in technical advances like AI

and multi-colour printing, and in price innovation, is coming out of China.

Bambu Lab continued to lead in global market

share, with the top four vendors in the category, Bambu Lab,

Creality, Elegoo, and Anycubic, collectively accounting for 88% of

all printers shipped globally in the period. The strongest YoY

shipment growth came from Flashforge, which saw printer shipments

jump over 120% in the price class in the period. Demand is

increasingly driven by massive "print farms" across the

globe, from China to the US, serving as a vehicle for "local

production" leveraging these Chinese-made machines. The period

also saw Creality go public on the Hong Kong Stock Exchange on

29-MAY-26, the first consumer-centric 3D printing company to do so.

*Price classes: Entry-level <$2,500;

Professional $2,501 to $20,000; Midrange $20,001 to $100,000;

Industrial above $100,000